Supply and demand projections show a gap in late-stage startup funding, especially in Series B. See how founders can prepare for the growth equity capital gap

.svg)

Paulo Passoni not only watched the development of Latin American startups from a prime seat: he played an essential part in it. Paulo was SoftBank's managing partner in LatAm for years, leading the largest fund for tech companies ever seen in the region. As part of that same journey, he also advised companies such as Creditas, Loggi, QuintoAndar, and VTEX.

While cooking up his next thing for Latin America, Paulo has been reflecting on the state of the Latin American startup ecosystem. One of these reflections has been making rounds on LinkedIn: a supply and demand projection for venture capital and growth equity capital in LatAm.

And what does it show? We're walking into a new valley of death. And we're not talking about the supply crunch we saw between Seed and Series A rounds a few years ago. The valley's in Series B.

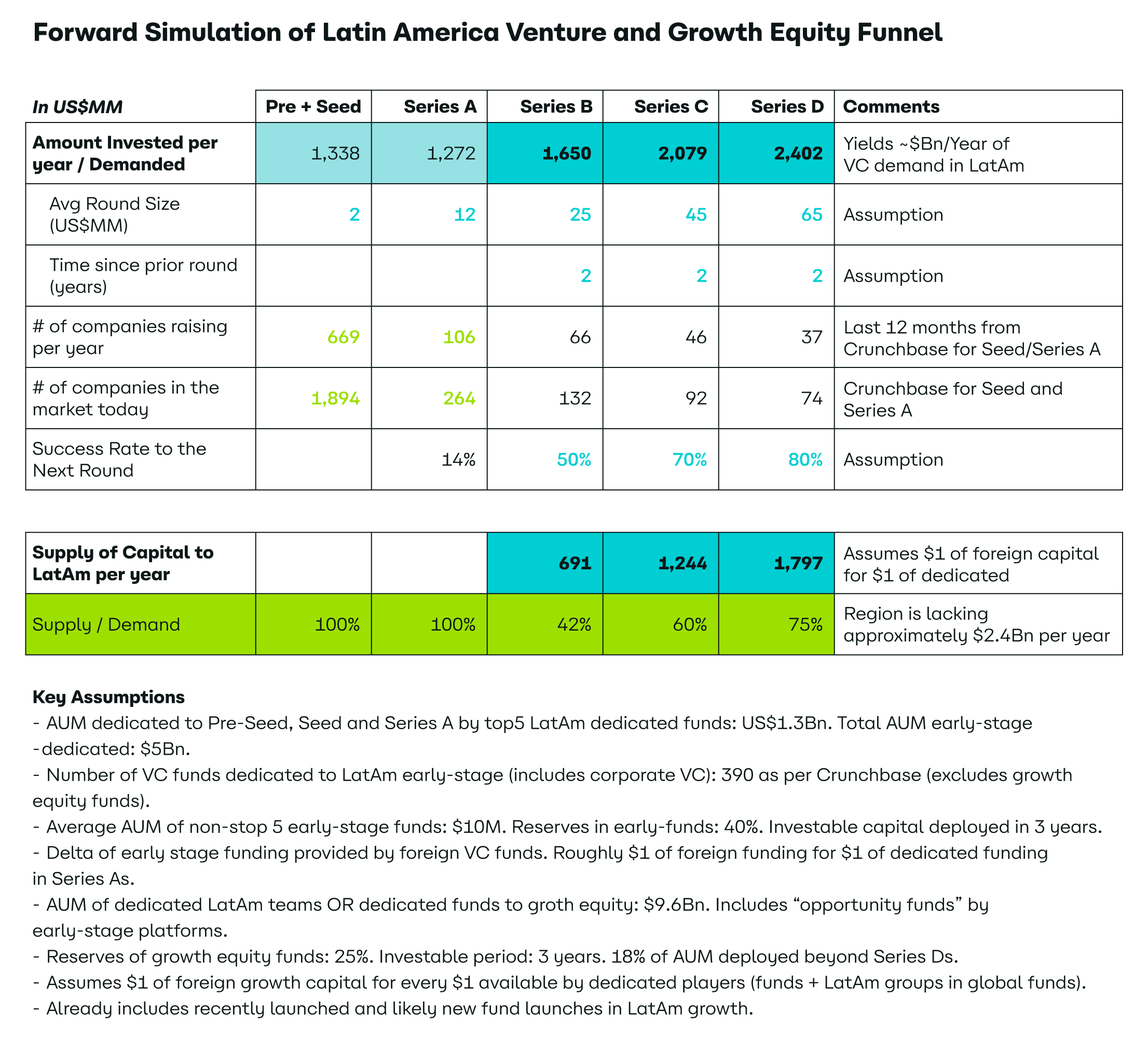

There's a total demand of US$ 8.7B in startup investments per year, versus a total supply of US$ 6.3B. And that means there won't be money for every founder that demands it. But we can be a little more specific: the supply looks pretty stabilized for early-stage startups, which are raising pre-Seed, Seed, and Series A rounds. The gap shows itself in the late stage, from Series B onwards.

"The market has evolved a lot in the early-stage side, but not on the growth equity side. And that's a problem", Paulo says. Here's what can happen in the Latin America venture capital and growth equity market, what challenges we'll face, and how you can prepare as a startup founder in LatAm.

Here are Paulo's projections for supply and demand for venture capital and growth equity capital in Latin America in the next few years:

Let's get into more detail. The projection's first line shows the investment demand in each startup round, considering some assumptions in average round size and time since the prior round. From pre-Seed to Series D, there's a total of US$ 8.7B in money startups need to keep thriving each year.

Paulo also projected how much supply there is each year for these startups. The calculation considers both funds dedicated to Latin America and "foreign opportunistic capital".

General Atlantic is a global firm with a dedicated team for LatAm, for example. Other funds don't have these teams and provide capital to regional startups occasionally. When we see a late cycle and therefore fewer opportunities in the US, these opportunistic funds might invest more in Latin America.

We had a late cycle in the past few years that ended with the meltdown in 2022, Passoni says. Now he assumes that we'll see just as much foreign capital as LatAm dedicated capital. A dollar for a dollar.

All of this leads us to the bottom line. We see that the total supply covers the demand for pre-Seed, Seed, and Series A investments. But that's not the case for Series B, C, and D. Series B is suffering the most – we'll explain why in a few seconds.

"The early-stage market has been developing quickly in the past few years, while the growth market evolves at a slower pace. Only 23S was launched to fill the gap since the market diminished its investment in Latin America. To fill the gap, we'd need about five growth equity capital funds", Passoni says.

The solution for this gap is simple to say but hard to do: develop the growth equity capital scene in Latin America, and Series B will tag along with it. For that, established firms need to create their growth equity branches, or start proving them if they're already operating.

"When you start a new fund, you raise only part of the assets you aimed for in order to first prove what you're doing to your investors. The best way to fill the gap is to have funds with a Series B thesis show stellar returns. Evidence of good performance will be the main driver for growth. The thing is that it will happen a little bit every year, for years. This gap won't be filled quickly", Passoni says.

Until these huge returns come into the scene, challenges remain for growth equity capital players and aspiring players looking at investing in Series B.

The first obstacle to creating and establishing late-stage funds is that much more capital is needed. It's easier to raise an early-stage fund of US$ 10M to US$ 50M than to raise a growth equity fund of US$ 500M

This additional amount is needed because it takes more capital to lead a Series B round. Why not raise the same as an early-stage fund and invest in fewer startups then?

Well, our second obstacle enters the scene. Unlike tech companies raising Series C+ rounds, startups at the Series B stage aren't as mature and close to breaking even to make a smaller portfolio viable in terms of risk.

"That's why growth equity capital goes to many places and Series B only makes up about 20% to 30% of the AUM [assets under management]. It's very risky to manage a fund that only does Series B", Passoni explains.

A third obstacle is one well-known by our friends at the earlier stages: liquidity. Series B is a ten-year bet, and an important metric for every fund is how much it has distributed back to its investors. So here's another incentive for growth equity capital to opt for Series C+ rounds. "The later I invest, the quicker I have liquidity. Valuation growth isn't the only metric that matters."

First and foremost: as a founder, you should assume that raising your Series B will be hard in the short to medium term. If we're only supplying 42% of the demand, that means that only one out of two companies that are raising will actually get their check.

Early-stage founders should keep their eyes on firms that also have a growth branch that could help raise next rounds, such as Kaszek, Monashees, and Valor. Founders should also consider raising funds abroad, after analyzing how much time they can and should dedicate to fundraising.

The consequences aren't restricted only to those raising their Series B, though. Some funds that invest early aren't considering that their returns can be diminished due to this lack of growth equity capital, Passoni says.

This lower multiple can come from mortality but also from less interesting exits. "If a startup does not receive enough capital to continue its journey, it can force itself into a strategic sale before the expected time for exit. It's selling or shutting down."

Lower multiples mean that investors will want to pay less for their investment to begin with, wishing to maintain their proportion of upside (e.g. 3X, 5X, 10X, etc.). Founders should be prepared to see more conservative valuations, trickling down from later stages to earlier stages.

In practical terms: you'll have the same dilution because you can't afford to give up too much of your startup equity (DON'T!), but you'll raise less cash for it. Therefore, you have less money to build your company.

And the drop in market caps hasn't been as fast as predicted by Paulo so far. He expects Latin America to still see more valuation crunch.

You're probably facing a huge headache right now. You're welcome.

Seriously now: as always, there's a light at the end of the tunnel. Boom and bust cycles tend to shorten with time in every industry since we understand better each cycle's behavior. After the meltdown last year, Latin America is in the early innings of a new cycle (and it might develop more quickly than you imagine).

If you need a check right now, though, you have to understand the current investor sentiment and adapt. In this scenario of a short supply of capital for late-stage startups and scale-ups, VCs will value companies that are efficient with money (and better yet if they don't need a lot of capital to thrive).

Look not only at your unit economics but at your full balance sheet, having cash flow and proximity to break-even as priorities. If before you'd only worry about that when you were raising a Series C, now profitability needs to be on your horizon even at the Series A round. If you don't worry about it, you’ll always be depending on external funding – and you might be left to dry at times like these.

"The more you step on the pedal, the more interesting your business becomes but the more you lose control of your destiny as an entrepreneur. It's the risk-return tradeoff every founder faces", Passoni says.

You can imagine how investors will also be paying attention to that tradeoff and opting for less capital-intensive bets. "Winner-takes-all markets probably won't be a priority for investors. VCs are looking less to B2C and high-spending businesses like iFood competitors, and more to B2B2C/B2B and low-spending solutions, such as softwares like Gympass", Passoni exemplifies.

Then, should everyone build a SaaS? Well, it's not that simple. Your solution also needs to address a sizeable market to nab growth equity funds.

If everyone had their software, going niche would be inevitable. It would be hard to find companies that could eventually provide for a billionaire market, and therefore have a relevant multiple of return over investment. Having a bunch of small startups that will never go public doesn't attract growth equity capital firms – we'd again be falling into the strategic sale and lower multiple on exit problem.

So you should stick with the problem and market you believe in, its solution being software or not. But always stay focused on efficiency.

Let's remember you will probably have less money for the same equity dilution. No wonder everybody's excited about artificial intelligence: it's a way to simplify tasks such as simple coding. Spend your resources on what AI can't do: have the necessary creativity to build your brand and educate your market. "If I had a new startup, my key hire would be someone that knows how to do marketing without an extensive budget", Passoni reflects.

.svg)

Disclosures for Latitud Finance

Latitud is not a bank. Banking, brokerage, FX, and other regulated activities are provided by our licensed partners in the United States and Brazil.

To become a Latitud Finance customer, you must agree to Latitud Finance’s Privacy Policy and Terms of Use.

Disclosures for US-Domiciled Latitud Finance Business Accounts

Some services that are part of your Latitud Finance Business Account are offered through Synapse Financial Technologies, Inc. and its affiliates (collectively, “Synapse”). Synapse is not a bank and is not affiliated with Latitud, Inc. Brokerage accounts and Cash Management Services are provided by Synapse Brokerage LLC (“Synapse Brokerage”), a registered broker dealer and member of FINRA and SIPC. You can find additional information about Synapse Brokerage on FINRA’s BrokerCheck. Please see Synapse’s Terms of Service, Privacy Policy, and the applicable disclosures and agreements available in Synapse’s Disclosure Library for more information.

Synapse Brokerage is a member of SIPC, which protects securities customers of its members up to $500,000 (including $250,000 for claims for cash). Funds maintained in the Synapse Brokerage Cash Management Program are deposited into one or more banks (“Program Banks”) where the funds are eligible for FDIC insurance up to $250,000. Please see your Brokerage Account Agreement and Synapse’s Terms of Service for further details. You can find a list of Partner Financial Institutions participating in a Synapse cash management program here.

.png)